Growing up I played soccer for many seasons and I always hated the first few weeks of practice. No matter how many seasons you had played, the first few weeks of practice were always spent going back to the basics. You spent time dribbling, practicing passing with your teammates, practicing headers, etc. when all I wanted to do was compete. I wanted to scrimmage and work on plays and strategy, but the coaches knew that you had to master the basics and the fundamentals before you could progress to the next level. They knew that if you just started competing it could enforce bad habits that would hinder you and keep you from progressing.

All of the above to say there are two more numbers that I track that are basic to FI. These two numbers are savings rate and net worth. As you begin to figure out what your saving rate and net worth are, just as I said with tracking your expenses, it is imperative that you don’t judge yourself. No matter what you have done in the past, and what your current savings rate and net worth are, commit now to making a change. This is your journey!

Your savings rate is exactly as it sounds. It is the amount of your income that you save over a certain period of time. While you can calculate your savings rate for any period of time, I personally track mine by year. In 2016 I had a savings rate of 53%, 2017 was 67%, 2018 was 48%, and so far this year I am at a 47% rate. The exciting thing about the savings rate is the higher the percentage the more money you have to put towards your freedom. The higher the percentage the more money you have to eliminate debt, to build your emergency fund, and to invest. The way I calculate my savings rate is to take my total W2 net income (aka post tax), subtract it from my credit card statements (expenses) to get my total dollar savings, and then dividing that by my net income to derive my savings rate.

((Net Income – Expenses)/Net Income) x 100 = Saving Percentage

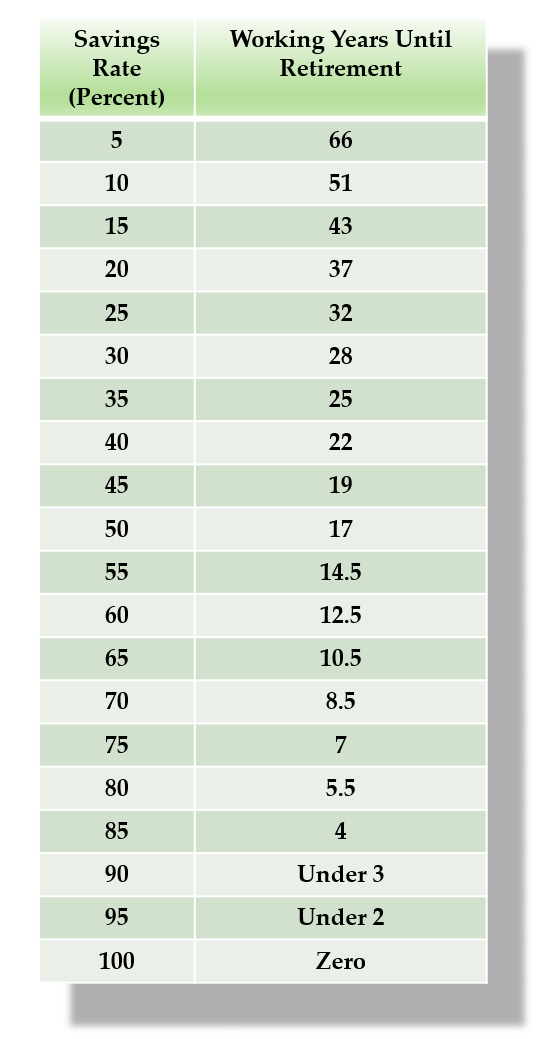

Calculating your savings rate this way is very much a back of the envelope way of doing it and does not tell the full picture as it leaves out 401K contributions (employer and personal contributions), income from side hustles, and any expenses I have in cash. I am personally fine with this as I mainly use this number to make sure my spending is not getting out of hand year to year and to challenge myself to do better. If you want to go down the rabbit hole of the various ways to calculate your saving rate, and more accurate ways, I highly recommend this article. Speaking of buying your freedom, Mr. Money Mustache has this chart that shows how quickly you can retire at each savings rate*. If that’s not motivating I don’t know what is!!

The other number is your net worth. Your net worth is basically your financial health. The higher the number the better able you will be to handle whatever situation life throws at you. Think of it like a health meter in a video game, the larger and more full the meter the better off you will be in the game. This is why I feel it is imperative to not only know and track this number, but also to grow it by living a frugal lifestyle. In America we tend to think of how financially healthy someone is by how big of a house they have or how new of a car they drive, but the truth is usually the opposite. As discussed in the great book, The Millionaire Next Door, those with a large house or a fancy car usually have a low or even negative net worth as they are heavily leveraged to have the house and car, whereas it is those with a modest house and an older car that are financially healthy and are the actual millionaires.

Merriam Webster’s Dictionary defines net worth as, “the excess of the value of assets over liabilities.” To calculate your net worth you add up all of your assets and subtract your liabilities. Your assets include all cash on hand, money in savings/checking accounts, money in retirement or other investment accounts, current market value of your vehicle, and current market value of your house. There is debate in the community wether to include your house and car in your net worth calculation, but I do as you can sell them and turn them into cash. I do think it is good to have the mindset though that they are actually liabilities as they take money from you instead of providing you money during the time you own them, but think that mindset needs to exist outside of the net worth calculation. The liabilities to include in your net worth calculation are the amount on your credit cards, amount owed on your mortgage, amount owed on student loans, and any other debt you may have.

Thankfully technology has made compiling all these numbers significantly easier. Personally I use the app Personal Capital** to track my net worth as it gives me an easy way to see all of my accounts in one place, does all of the math for me, and updates daily. If you are uncomfortable giving an app access to your accounts you can find numerous net worth spreadsheets online or create your own. If you want to go real old school you can even buy some graph paper and go to town. Who remembers graph paper?!?!

As I mentioned last week, I fought tracking all these statistics for a while and am sad that I waited as long as I did. My senior year of college I was the technical director (TD) for one of our shows. It was my second time serving as TD and the first show had come together without a hitch. On this second show my mentor kept getting after me to sit down and make a build calendar to make sure the build was staying on track. I resisted because I didn’t see the need to take an hour away from building and supervising my crew to create this document as myself and my peers were constantly working and in my mind making progress. As you have probably already guessed the set did not come together on time and the designer had to make some concessions to his vision. To me tracking your expenses, your savings rate, and your net worth are important because as the build calendar would have done for me, they give you metrics to track your progress and make sure you are staying the course. As always if you have any questions I am here to help!!

*To read the article from which the chart is taken go here.

**If you decide to use Personal Capital contact me and I can send you a referral code to potentially get us both a gift.

{kind=link}